Recently Scott Alman, Paul Shepherd and I took the opportunity to travel to the USA, to attend, amongst other meetings, a global investment symposium in Austin, Texas. In attendance were a number of the leading independent advisory firms from around the world.

Two days rubbing shoulders with advisors from the US, Canada, UK, and other parts of Europe really confirmed to me that Alman Partners are delivering world class investment solutions to our clients. Interestingly, in my observation, there are similar themes and challenges for all of our clients which we discussed in detail.

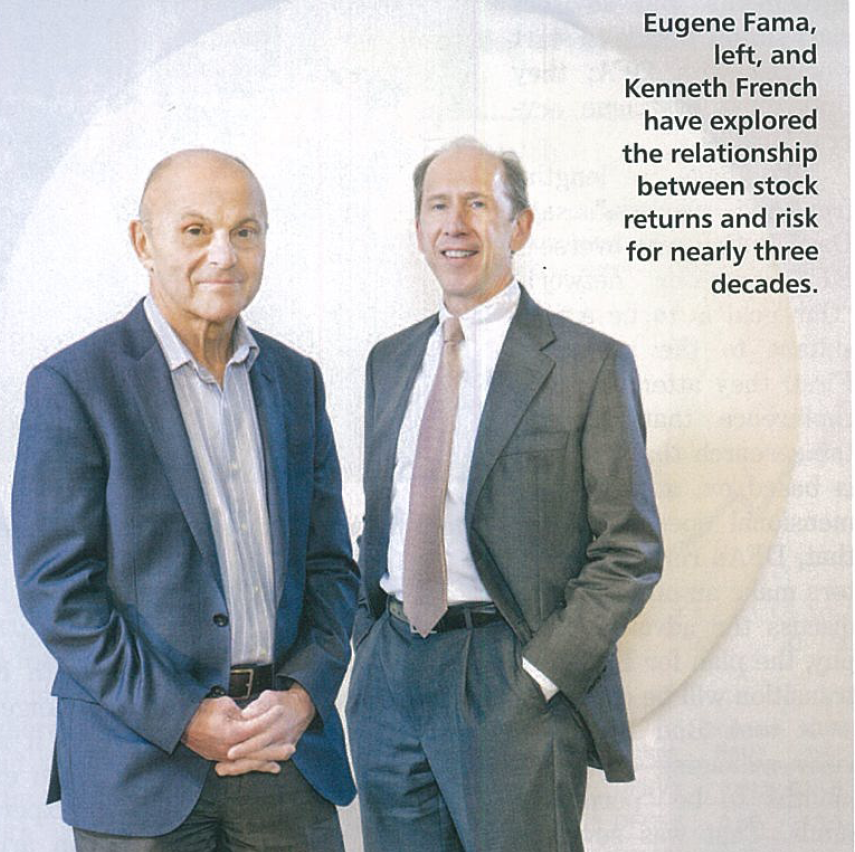

Undoubtedly the highlight of our time in Austin was a panel discussion with two of the brightest minds who pioneered the demystification of successful investing. Eugene Fama and Ken French had the easy banter of two brilliant minds that have collaborated and challenged each other for over three decades. Professor Fama recently won the Nobel Prize for his theory of market efficiency which he presented in 1965. In 1992 they teamed up and released a paper known as the Fama/French 3 factor model. This work is the foundation of the investment solutions here at Alman Partners.

I have summarised a few key points below:

The Wizard Behind the Curtain

Much of the financial services industry relies on the magic of picking winners and beating the market. According to Fama and French there are too many people relying on the idea of a “wizard behind the curtain” to perform “investment magic” in order to gain higher investment returns. The “wizard” or financial guru is supposed to have some special skill to pick the right markets, the right stocks, at the right time and with low risk. According to Fama and French this is a delusion. From Ken French’s perspective “there is almost no one in the academic world who believes in active money management”. According to French there is little evidence active managers can add value over any meaningful period of time.

Capturing Expected Investment Returns

Professor Fama commented that the key to achieving a successful investment outcome is to “build a well-diversified portfolio that captures the known dimensions of expected returns”.

On hedge funds

Just last week the California State Pension Fund announced that they had terminated the mandates of all hedge fund managers citing poor performance and high costs over an extended period of time. Asked to comment, Eugene Fama responded, “I have never been a fan of hedge funds that is on the public record. I think it is a zero sum game in which the hedge fund manager gets to charge a 2% fee with a 20% performance bonus. The fact that CALPERS is pulling back from hedge funds is a sign of intelligence”.

Eugene Fama is the Robert J. McCormick Distinguished Service Professor of Finance at Chicago Booth School of Business, University of Chicago.

Ken French is the Roth Family Distinguished Professor of Finance at the Tuck School of Business at Dartmouth College.

Stephen Lowry CFP, DFP, FAIM, is a representative of Alman Partners Pty Ltd, Australian Financial Services Licence No: 222107.

Note: This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.