As the FY27 Federal Budget looms, let’s take a look back at the changes presented at the last Budget and their ongoing impact on your pockets. When the FY26 Federal Budget was released back in March 2025, we learned that we were beginning the fiscal year in a deficit, wrapped in an uncertain economy, global trade wars and rising tariff tensions to boot.

Let’s break down what this means for you and what you should consider.

Tax

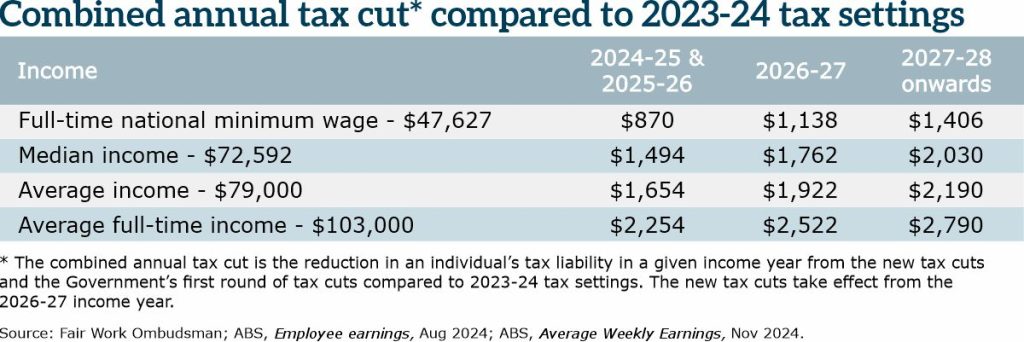

The Albanese Labor Government is delivering more tax cuts for every Australian taxpayer in 2026 and 2027, on top of the tax cuts that have been rolling out since 1 July 2024.

Every Australian taxpayer will receive an extra tax cut of up to $268 from 1 July 2026 and up to $536 every year from 1 July 2027, compared to the 2024–25 tax settings.

These new tax cuts are modest, but they will make a difference.

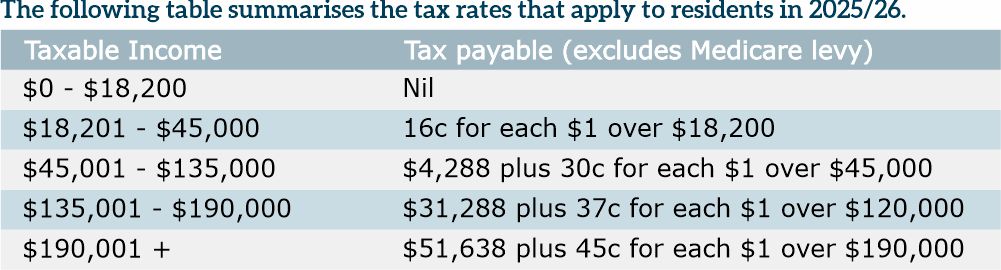

Last year, the Government cut two rates and lifted two thresholds to deliver tax cuts for all Australian taxpayers, including cutting the rate that applies to taxable income earned between $18,201 and $45,000 to 16 per cent.

The Government will cut income taxes further over two years:

- From 1 July 2026, this rate will be reduced to 15 per cent.

- From 1 July 2027, this tax rate will be reduced further to 14 per cent.

Combined with the first round of tax cuts from 2024-25, this means you can save $2,522 in tax in 2026-27, and $2,790 in 2027-28. Or $48.50 a week.

Healthcare & better wages for women

As of 1 January 2026, you won’t pay more than $25 for a medicine script covered under the Pharmaceutical Benefits Scheme (PBS), which was previously set to $31.60. Pensioners will continue to pay the locked-in fee of $7.70.

Aged care workers and childhood educators, a predominantly female workforce, can expect a boost to earnings in this sector.

Gender equality will now sit under the Fair Work Act 2009 to ensure the work of women is not undervalued in female-dominated industries.

Social Security

The cost of childcare means many parents, particularly mums, must forgo their careers or contribute a large portion of their salary to childcare fees.

As of 5 January 2026, all families – except those earning more than $533,280 – will get 3 days of subsidised childcare per week.

Super

Mandatory Payday Super

Employers must pay Super Guarantee contributions at the same time as salary and wage, aiming for compliance within 7 business days of payment, reverting from the current contributions being received by the employee’s fund by the 28th day after the end of each quarter.

Furthermore, the Super Guarantee Charge will apply to late payments, including a new “administrative uplift” fee.

Paying super more frequently means your money gets invested sooner, taking advantage of better long-term outcomes due to the power of compounding.

Increased Contribution Caps

Due to wage inflation, the annual concessional contribution cap will rise to $32,500 from $30,000, with corresponding increases to non-concessional caps to $130,000 p.a. from $120,000.

This creates opportunities to top up superannuation while reducing taxable income if making a salary sacrifice while building wealth towards your financial freedom goal.

Super on Paid Parental Leave

Superannuation will be paid on Government-funded Paid Parental Leave for babies born or adopted from 1 July 2025, with payments made annually to accounts starting 1 July 2026.

For families that have a baby arrival planned, while they may be eligible to receive government-paid maternity pay (subject to income tests), which is based on minimum wage, receiving super contributions helps to ensure that the gap of not working while raising a family doesn’t negatively impact the caring parent’s retirement funding.

How this may impact you personally?

The overall changes are positive and raise opportunities, such as a further reduction of taxable income via additional before-tax contributions (Concessional Contribution Cap will increase by an additional $2,500 p.a.), especially valid to consider if your taxable income starts tipping over to the next marginal tax rate.

This is in addition to an increased after-tax cap (increasing by $10,000 p.a.), which allows you to add towards your accumulation account in preparation for your retirement goals.

Most importantly, while the Consumer Price Index; (CPI) is predicted to increase from the current 3.8% by another 1% due to the current Middle East war, taking home more income in your pocket is something that everyone will appreciate.

Reach out to your adviser or team at Alman Partners on how the above impacts your specific situation and future trajectory of your goals.

Veronika Holubova (MFinP, GradCertFP, ADFP, DipFP) is an Employee of Alman Partners Pty Ltd, Australian Financial Services Licence No: 222107.

Any information provided to you was purely factual in nature. It has not been taken into account your personal objectives, situation or needs. The information is objectively ascertainable and is not intended to imply any recommendation or opinion about a financial product. This does not constitute financial product advice under the Corporations Act 2001 (Cth). It is recommended that you obtain financial product advice before making any decision on a financial product such as a decision to purchase or invest in a financial product. Please contact us if you would like to obtain financial product advice.